Memory Chip Shortage is becoming a growing topic across the semiconductor market as AI infrastructure expands rapidly. The global semiconductor industry entered a strong expansion phase in 2025, driven largely by accelerating demand for artificial intelligence systems. On February 26, 2026, Semiconductor Intelligence released a market report based on data from World Semiconductor Trade Statistics, analyzing semiconductor sales trends in the fourth quarter of 2025.

The report highlights a major structural shift across the semiconductor supply chain. Major memory manufacturers experienced exceptional growth as AI data centers rapidly expanded their computing capacity. Five major memory companies — Samsung Electronics, SK Hynix, Micron Technology, Kioxia, and SanDisk — recorded an average quarter-over-quarter growth of 27% in Q4 2025.

This surge reflects a fundamental change in semiconductor demand. Modern AI servers require massive volumes of high-performance memory and storage components. As a result, memory suppliers have become one of the fastest-growing segments of the semiconductor market.

For manufacturers and procurement teams, these shifts are more than industry statistics. They directly affect component availability, pricing stability, and supply chain planning. Companies that rely on stable semiconductor sourcing must increasingly monitor these market dynamics to prevent production disruptions.

Major Memory Manufacturers Achieved 27% Average Growth in Q4 2025

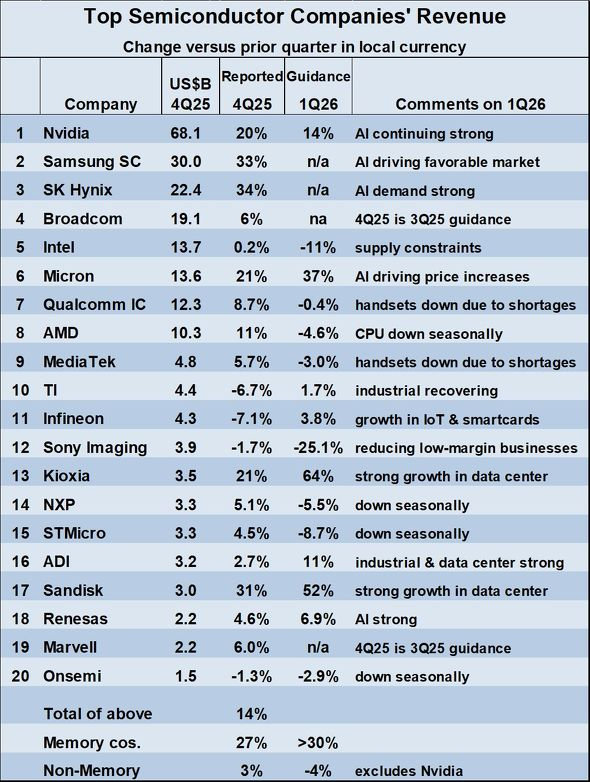

According to the ranking of the world’s top semiconductor companies by quarterly revenue, several memory manufacturers recorded strong growth in the fourth quarter of 2025.

| Rank | Company | Q4 2025 Revenue | QoQ Growth |

|---|---|---|---|

| 1 | NVIDIA | $68.1B | +20% |

| 2 | Samsung Electronics | $30B | +33% |

| 3 | SK Hynix | $22.4B | +34% |

| 6 | Micron Technology | $13.6B | +21% |

| 13 | Kioxia | $3.5B | +21% |

| 17 | SanDisk | $3.0B | +31% |

When combining Samsung Electronics, SK Hynix, Micron Technology, Kioxia, and SanDisk, the average growth rate reached approximately 27% during the quarter.

Two major factors contributed to this strong performance.

First, memory prices began recovering after a prolonged industry downturn during 2023 and 2024. Market estimates indicate that DRAM prices increased by roughly 40–60% throughout 2025, while NAND Flash prices rose by approximately 30–45%.

Second, the rapid expansion of AI computing infrastructure significantly increased demand for high-performance memory technologies. Modern AI servers often integrate 8 to 16 GPUs, each paired with high-bandwidth memory such as HBM3 or HBM3E.

For example, systems based on NVIDIA H100 GPUs typically include 80GB of HBM per GPU, meaning an eight-GPU AI server may require more than 640GB of high-bandwidth memory. Such configurations dramatically increase memory consumption compared with traditional computing systems.

Global Semiconductor Market Reached $792 Billion in 2025

The broader semiconductor market also experienced significant growth in 2025. According to statistics from WSTS, the global semiconductor market reached $792 billion, representing 25.6% year-over-year growth.

| Year | Market Size | Growth |

|---|---|---|

| 2023 | $527B | -8% |

| 2024 | $630B | +19% |

| 2025 | $792B | +25.6% |

This growth rate is the strongest since the 26.2% expansion recorded in 2021, when the industry rebounded following pandemic-related disruptions.

Among all semiconductor companies, NVIDIA reported the most significant increase, achieving 65% year-over-year revenue growth due to strong global demand for AI GPUs and data center computing infrastructure.

At the same time, the five major memory manufacturers collectively recorded approximately 29% annual growth, highlighting the increasing importance of memory technologies in modern computing systems.

Memory Chip Shortage From AI Demand May Impact Other Semiconductor Segments

While AI infrastructure continues to drive semiconductor demand, it is also creating supply allocation challenges across the industry.

AI servers require substantial volumes of DRAM, NAND storage, and high-bandwidth memory. As production capacity shifts toward these high-value applications, other sectors may experience tighter component supply.

For example, Intel expects its Q1 2026 revenue to decline by 11% compared with the previous quarter, partly due to limited availability of PC memory components.

Similarly:

- Qualcomm forecasts a 0.4% decline

- MediaTek expects around 3% revenue decline

According to research from International Data Corporation (IDC), ongoing memory shortages could result in PC shipment declines of 2–4% and smartphone shipment declines of 1–3% during 2026.

These changes highlight how AI-driven demand is beginning to reshape semiconductor supply priorities across the entire industry.

What This Means for Component Procurement

For many small and mid-size electronics manufacturers, semiconductor market shifts translate directly into component sourcing challenges.

When memory demand surges due to AI infrastructure expansion, procurement teams may encounter several common risks:

- Longer lead times for memory and related components

- Higher pricing volatility

- Limited spot market availability

- Reduced supplier allocation for smaller orders

In such conditions, companies often benefit from working with multiple component sourcing channels rather than relying on a single distributor.

Suppliers such as 7setronic support overseas manufacturers by helping locate available semiconductor inventory across global supply networks. This approach allows procurement teams to maintain stable production schedules even when certain components become difficult to source through traditional distribution channels.

Semiconductor Market Outlook for 2026

Industry analysts expect the semiconductor market to remain strong in 2026, primarily supported by three major sectors:

AI and Data Center Infrastructure

Global cloud providers continue expanding AI computing capacity. Industry estimates suggest that AI infrastructure investment may grow by more than 30% annually over the next several years.

Automotive Electronics

Electric vehicles and advanced driver-assistance systems require increasingly complex semiconductor architectures. A modern EV may contain $1,000 to $1,500 worth of semiconductor components, including power devices, sensors, and computing processors.

Industrial Automation

Factory automation, robotics, and smart manufacturing systems continue to generate stable semiconductor demand across global industrial markets.

Even if consumer electronics markets experience short-term fluctuations, these sectors are expected to support continued semiconductor industry growth.

According to industry forecasts, the global semiconductor market may expand by more than 20% in 2026, reinforcing the long-term importance of AI-driven computing infrastructure.

FAQ

Why are memory manufacturers growing so quickly?

AI servers require large volumes of DRAM and high-bandwidth memory, significantly increasing demand for memory components.

Will AI demand affect PC and smartphone production?

Yes. Increased AI memory consumption may tighten supply, which can influence PC and smartphone production volumes.

How fast will the semiconductor market grow in 2026?

Industry forecasts suggest global semiconductor revenue could grow by more than 20%.

- How the AI Server Supply Chain Is Reshaping PCB, MLCC, Copper Foil and Electronic Glass Fiber Markets

- Top 12 Global MLCC Manufacturers in 2026: Financial Performance, Market Position and Supply Chain Trends

- NVIDIA Rubin BOM Analysis: What Component Buyers Need to Know Before the Next AI Hardware Wave

- Semiconductor Traceability vs Date Code: Can Older IC Inventory Still Be Reliable?

- From Components Sourcing to PCB Assembly: How 7SEtronic Supports OEM & EMS Projects