7SEtronic is a Shenzhen-based company that supports OEM/EMS and device makers with electronic components sourcing, BOM cost optimization, alternative parts solutions, and PCBA assembly services.

The insights in this article are based on real market observations, sourcing experience, and daily engagement with the global electronics supply chain.

About the author: Mr. Takashi Yujino is the director of the Japan Precision Machining Research Institute. He has long been engaged in semiconductor research and development at the forefront of Japan’s manufacturing industry. He received his Ph.D. in Engineering from Kyoto University in 2000. Since then, he has been engaged in teaching, research, consulting and journalism related to the semiconductor industry. He has written books such as “The Failure of Japan’s Semiconductor Industry”, “Lessons from the Collapse of ‘Electrical Machinery and Semiconductors'”, and “Lost Manufacturing Industry: The Defeat of Japan’s Manufacturing Industry”.

In recent years, many have viewed the expansion of AI-related investments as evidence of a bubble, but the Generative AI Semiconductor Trends show that this growth is driven by structural demand rather than speculation.

01. Artificial Intelligence Is Not a “Bubble”

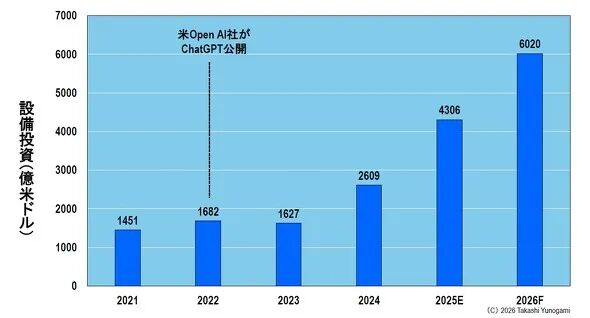

The capital expenditure (Capex) of cloud service providers has already expanded to a scale that can no longer be described with the mild term “rapid growth.” The top eight cloud providers’ equipment investment is expected to grow from $145.1 billion in 2021 to $602 billion in 2026, more than a fourfold increase. This growth clearly exceeds common expectations.

Even so, some still whisper: “It’s just another bubble.” “It will collapse someday.” This is a familiar, escapist narrative. But such judgments lack factual basis, and they don’t even qualify as optimistic speculation—they are simply psychological self-comfort. This time, the investment expansion is not driven by sentiment, speculation, or economic boom, but by computational demand on an entirely different scale—a force almost akin to a law of physics.

The decisive difference lies in the fact that the computational load of generative AI is not an “extension of search,” but exists in a completely different dimension of “training and inference.” As explained later, Google Search relies primarily on CPUs, whereas ChatGPT inference is centered on GPU-based large-scale matrix computations, with computing demands 10,000 to 100,000 times greater.

For this reason, cloud providers do not “choose” to increase investment—they must, or risk being outcompeted. A cloud platform incapable of running generative AI ceases to have value. Thus, the investments will not stop; more accurately, they cannot stop.

This article argues that what is happening now is not the so-called “AI bubble,” but an “AI trend” that will irreversibly shift the center of the semiconductor market.

02. Cloud Computing Investments Are Expanding at an Extraordinary Rate

First, let’s face reality. Figure 1 shows the equipment investment trends of the top eight cloud service providers, including Amazon (AWS), Microsoft (Azure), Google (Google Cloud), Meta (Facebook), Oracle (OCI), and China’s Alibaba Cloud, Tencent Cloud, and ByteDance.

Figure 1. Equipment Investment of the Top 8 Cloud Makers; Source: Compiled by the author based on TrendForce data.

As noted, these eight companies’ equipment investments are expected to grow from $145.1 billion in 2021 to roughly $602 billion in 2026—a more than fourfold increase. This is no longer just “growth,” but an acceleration.

Although there was a slight decline between 2022 and 2023, this should not be underestimated. Observing the growth trend after 2024 shows that cloud providers have been advancing “step by step.” This investment boom coincides with the release of ChatGPT by OpenAI in the U.S.

In other words, they invest in generative AI not because it is the “next gold mine,” but because generative AI, as a “game-changer” for existing infrastructure needs, forces them to invest.

The factors driving cloud investment expansion are numerous: data center construction, land, electricity, cooling, networks, storage, security… but if one thread runs through them, the essence is clear—computational power demand. The explosive growth of computational demand drives all associated costs upward. Essentially, cloud investment expansion is a large-scale battle over computing resources.

Currently, the demand for computing power cannot be explained as a mere extension of traditional web or search services. Generative AI does not simply ask the cloud platform for “a bigger appetite”; it demands the entire “stomach” itself to be fundamentally enlarged.

03. Google Search vs. ChatGPT: Similar in Appearance, Completely Different in Reality

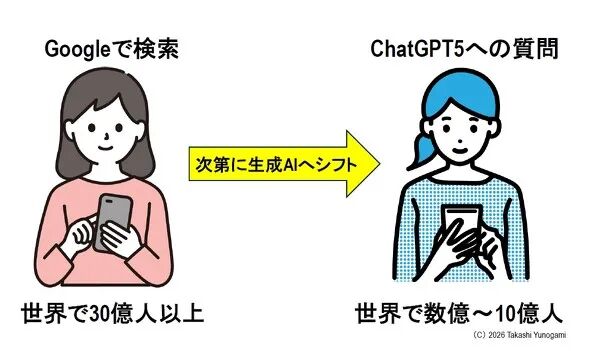

Here, it is important to correct a common misunderstanding: “From a user perspective, isn’t Google Search just like generative AI—ask a question and get an answer?”

Indeed, as shown in Figure 2, user actions are similar. Whether Google Search or generative AI, human behavior is nearly identical. Yet, Google Search, with over 3 billion users worldwide, is gradually being replaced by generative AI like ChatGPT, whose user base continues to expand toward 1 billion.

Figure 2 shows the actions a human performs when conducting a Google search and asking a ChatGPT5 question.

Personally, I started using ChatGPT’s paid version last year, and my Google Search frequency has significantly decreased since. The reason is simple: ChatGPT is more convenient. The growing awareness of generative AI’s convenience explains its continuous user growth.

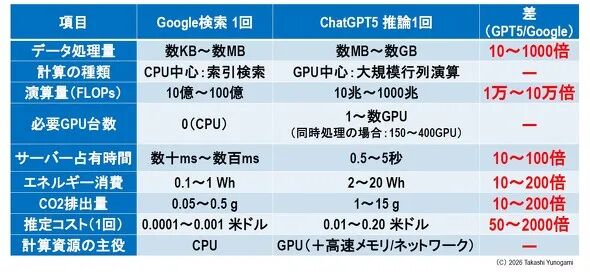

The key point is this: even for the same “question,” the computation performed in the cloud by Google Search and by ChatGPT is completely different.

Figure 3. Comparison of calculations for a single Google search and a single ChatGPT5 query; Source: Based on the author’s investigation and speculation.

This decisive difference is shown in Figure 3. Google Search is primarily CPU-centric indexing, while ChatGPT inference is GPU-centric large-scale matrix computation. In terms of FLOPs (floating-point operations), Google Search is on the order of 1 billion to 10 billion, whereas a single ChatGPT inference reaches 10 trillion to 1 quadrillion—10,000 to 100,000 times higher. Moreover, compared to Google Search, ChatGPT requires 10 to 100 times more server time, 10 to 200 times more power, and produces 10 to 200 times more CO₂ emissions. The estimated cost per inference is 50 to 2,000 times higher.

In short, generative AI is not “an advanced search.” It is a fundamentally different computational paradigm with an entirely different load. The widespread adoption of generative AI means that the “computational units” handled by cloud platforms are rapidly expanding. This cannot be solved by price cuts, negotiation, or sales skills—it is a physical reality, requiring AI chips like GPUs, electricity, cooling, high-speed networks, high-bandwidth memory (HBM), and even advanced packaging and interconnect technologies.

A common market refrain is: “Computing efficiency will improve, and the load will lighten.” Efficiency will indeed improve, but the pace of generative AI adoption, usage frequency, and model evolution far outpaces efficiency gains. Even if a single computation becomes lighter, if overall usage grows tenfold, total computing demand rises. Considering longer inputs, longer outputs, and the rise of image and video inference, computing loads will only grow heavier.

Thus, the reason cloud investments continue to expand is not “overheating” or “blind optimism,” but a fundamental shift in computing demand structure. If investment stops, failure is guaranteed. Cloud providers increase investment not out of courage, but out of fear—the fear of being left behind forces them to floor the accelerator.

04. AI Is Fundamentally Different from Past Bubbles

Now, the core question: is this a bubble?

The answer: calling this a “bubble” is entirely wrong. Past bubbles differ fundamentally in the nature of their demand. Let’s quantify this.

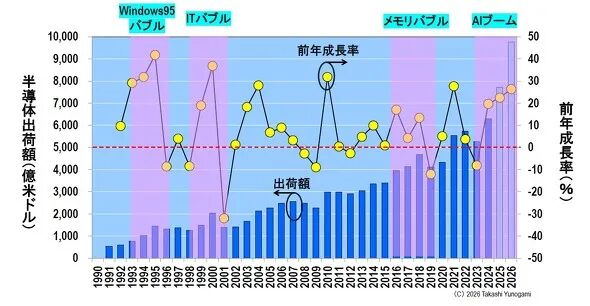

Figure 4 shows global semiconductor shipment values and year-over-year growth rates, marking the Windows 95 bubble, the IT bubble, and the memory bubble. A common feature of past bubbles is rapid growth followed by a sharp decline, driven by “short-term demand spikes” and “inventory adjustments.”

Figure 5A compares year-over-year growth from year N to N+3 for the Windows 95 bubble, IT bubble, memory bubble, and the current AI boom (temporarily called the “boom”). Figure 5B shows: the Windows 95 bubble grew 41.7% before dropping to -8.6%; the IT bubble went from 36.8% to -32%; the memory bubble from 13.4% to -12%. The cyclical pattern of “rapid rise—sudden collapse” is clear.

Data source: Compiled by the author based on WSTS data.

In contrast, the generative AI boom shows: -8.1% in 2023, 19.7% in 2024, 22.5% in 2025, with almost certain positive growth in 2026. Many industry experts note that before 2030, generative AI demand is highly unlikely to decline.

In other words, what is happening is not a “bubble,” but a single, extremely large, and extremely strong “trend.”

Unlike past bubbles, demand is not driven by one-time consumption cycles such as “PC adoption” or “smartphone replacement cycles.” The demand for computational power is being infrastructuralized. Generative AI is not a product that ends once sold—it is embedded into nearly all business processes, integrated into services, and forms the productivity foundation of enterprises. This foundation is built on extremely heavy computation. In this context, cloud investment is no longer “heat in a business cycle,” but a structural feature of society.

Calling generative AI a “bubble” is essentially escapism, relying on past experience. What is happening now has no precedent in any industrial textbook.

05. Generative AI Semiconductor Trends Outlook Toward 2030: Investment Growth

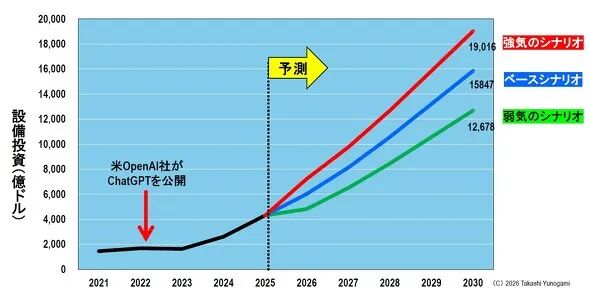

How far will top cloud providers’ equipment investment expand? Figure 6 provides predictions for Top 8 cloud providers’ data center investments under pessimistic, baseline, and optimistic scenarios. Even under pessimistic assumptions, investment continues to accumulate. This is because generative AI is no longer a “luxury add-on” but a basic requirement for competition.

Figure 6. Data Center Investment Forecasts of the Top 8 Cloud Service Providers; Source: TrendForce press release and author’s forecasts.

The harsh reality of cloud competition in the generative AI era is that reducing investment does not improve profit margins. Falling behind in AI performance leads to losing customers, and eventually the platform itself. Slowing investment is thus closer to a declaration of failure than rational management.

Investment recovery is difficult: GPUs are expensive, HBM is costly, power supply is tight, cooling is challenging, and supply chains are complex. Yet investment cannot stop because a structural reality has emerged: participants without computing power are eliminated.

Ultimately, cloud computing investment is no longer “betting on the future,” but “defending the present.” Given this structure, sustained investment growth through 2030 is almost inevitable.

06. Rapid Expansion of the Logic Chip Market for Data Centers

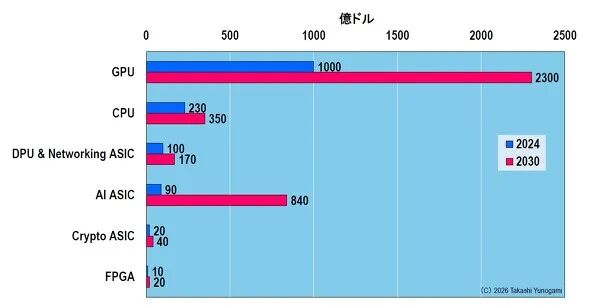

Continued cloud investment directly drives overall semiconductor market growth. Logic chips for data centers are the most certain growth area.

Figure 7 shows the market forecast for data center logic from 2024 to 2030. GPU market size will grow from $100 billion to over $230 billion, doubling. AI ASIC market size is projected to surge from $9 billion to $84 billion, a 9× increase.

Figure 7. Market Forecast for Logic in Data Centers (2024-2030); Source: Primarily based on forecast data from Yole Group, compiled by the author.

Importantly, generative AI will not remain dominated solely by NVIDIA GPUs. Hyperscalers avoid reliance on a single supplier to maintain price negotiation power. Therefore, they are shifting toward AI ASICs for cost-effective performance gains, with Broadcom taking on significant design work.

The AI semiconductor market will evolve into a dual-pillar structure: GPU as the core, with AI ASICs (e.g., Broadcom) growing rapidly alongside. Even if GPUs remain the mainstay, AI ASICs will see rapid expansion—this is the reality of the data center logic market.

07. Memory Will Remain in Long-Term “Supply Shortage, High Price”

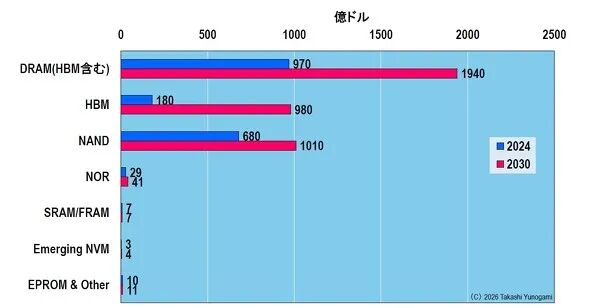

Among all semiconductor categories consumed by generative AI, memory is hit the hardest. Figure 8 shows the memory market forecast from 2024 to 2030: DRAM grows from $97 billion to $194 billion, nearly doubling; HBM will reach $98 billion, occupying half of DRAM by 2030. This indicates a structural shift in memory market leadership.

Figure 8 Storage Market Forecast (2024→2030); Source: Primarily based on forecast data from Yole Group, compiled by the author.

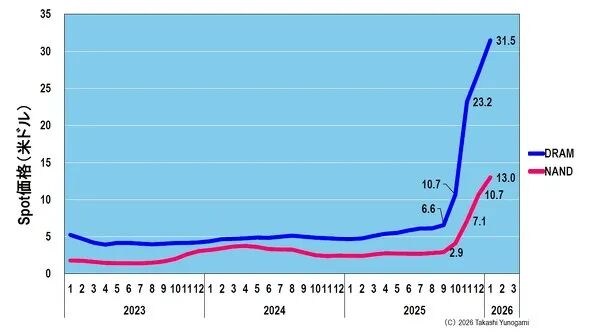

Figure 9 shows DRAM and NAND spot prices rising sharply from 2023 to 2026. Old rules—“price rises → expand capacity → market stabilizes”—no longer apply. Expanding HBM is difficult: yield improvement is challenging, advanced packaging is required, equipment and material constraints abound, and supply cannot easily catch up with demand. Memory manufacturers focus resources on AI servers, which have higher margins. As a result, general-purpose storage for PCs and smartphones is compressed, pushing prices up.

Figure 9. Upward trend of DRAM and NAND spot prices; Source: Compiled by the author based on TrendForce data.

Memory shortages will persist, and prices will remain high—this is likely the new normal in the AI era. Personally, I replaced my PC last December after six years, partly due to rising DRAM and SSD prices likely to continue. The rational choice is to buy early, while inventory exists, to avoid later price surges.

08. TSMC’s “Revenue Driver” Shifts from N5 to N3

Riding the AI wave, TSMC is likely the most effective and profitable semiconductor manufacturer. Figure 10 shows TSMC revenue by process node, highlighting a shift from N7 to N5 and now to N3.

Figure 10. TSMC’s revenue by node in each quarter; Source: Compiled by the author based on TSMC Historical Operating Data.

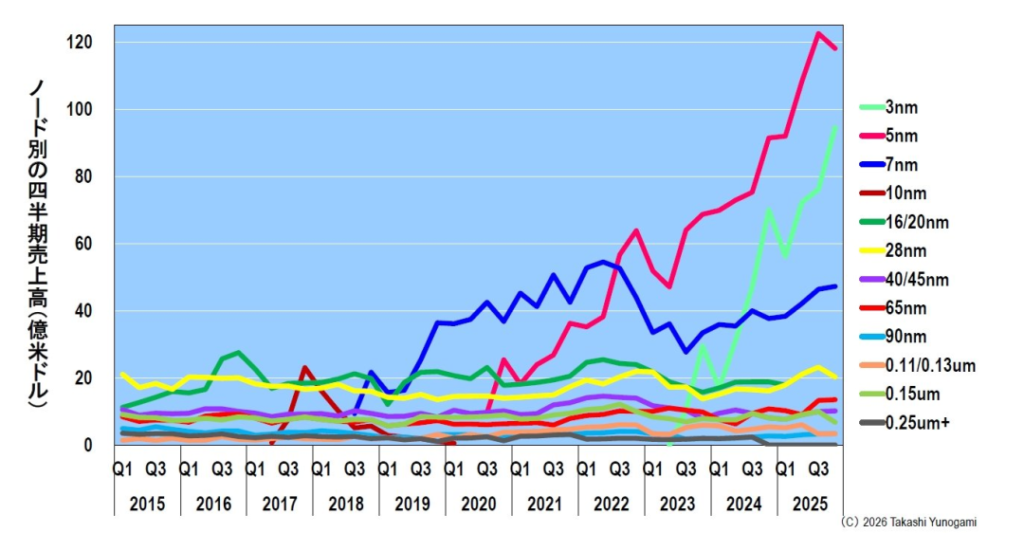

Figure 11 shows wafer starts by node: only N5, N3, and N2 are growing; other nodes decline. This is not a slogan—it reflects reality: only advanced nodes are expanding. Generative AI requires enormous computation, relying on high-performance AI chips supported by advanced nodes. Currently, TSMC is almost the sole provider meeting this demand, becoming the industry’s “center of gravity.”

Figure 11. TSMC’s wafer starts by node in each quarter (Q4 2025 is a forecast); Source: Claus Aasholm, “One Peak short of Twin Peaks”, Semiconductor Business Intelligence, data as of October 22, 2025, and the author’s calculations.

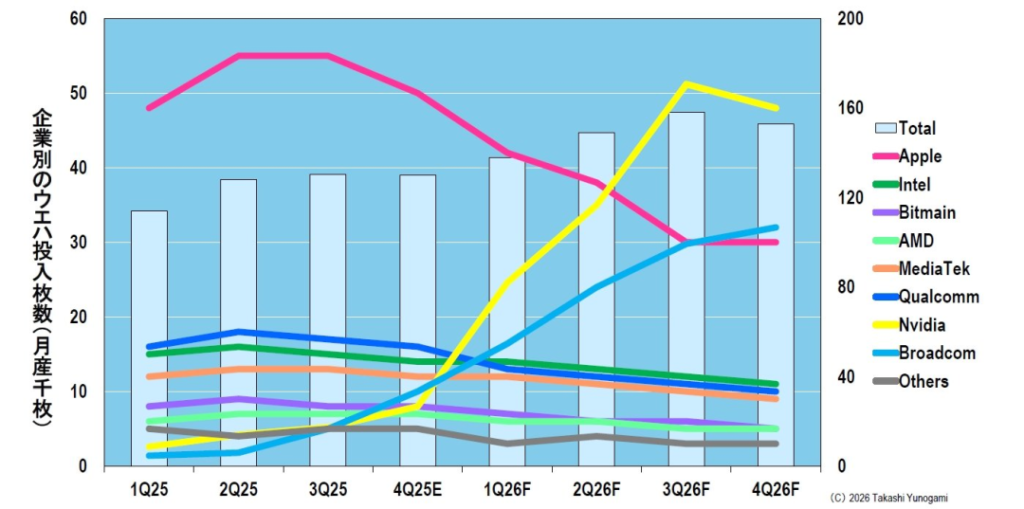

09. N3’s Main Players: From Apple to NVIDIA and Broadcom

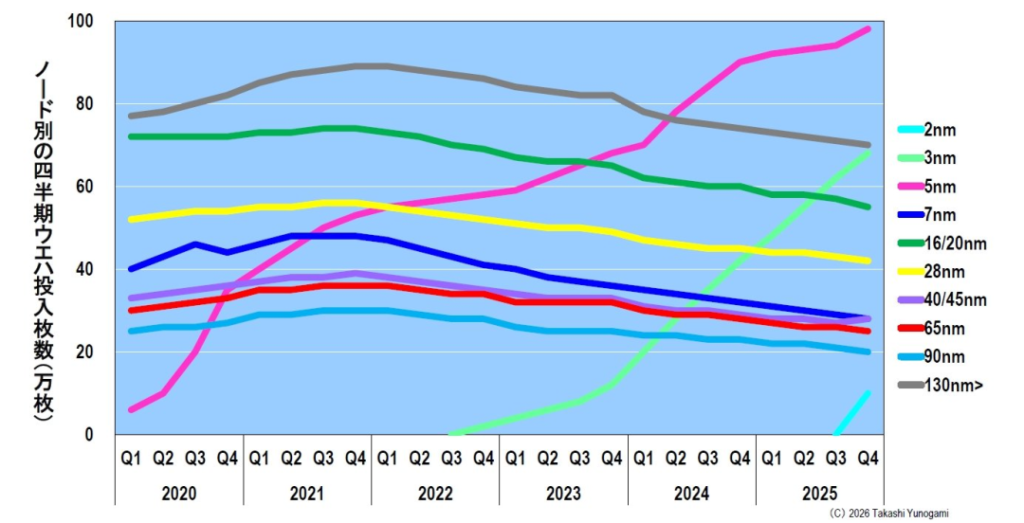

Historically, Apple was the largest driver of TSMC’s advanced nodes, but this is shifting. Figures 12 and 13 show wafer starts on N3 by customer, predicting that NVIDIA and Broadcom will surpass Apple in 2025–2026. This signals a shift from “smartphone processors driving advanced nodes” to “AI chips driving advanced nodes.”

Figure 12. TSMC’s 3nm process wafer input forecast by company (equivalent to 1000 wafers per month); Source: Based on data from Joanne Chiao’s seminar “2026 Outsourcing Market Outlook – Advantages of Advanced Processes and Saturation of Mature Processes” (December 16, 2025) on TrendForce, compiled by the author.Figure 13. TSMC’s 3nm process wafer input forecast by company; Source: same as above.

Apple uses advanced nodes to enhance consumer experience; NVIDIA and Broadcom use them to dominate cloud computing—a significant difference. AI chips are persistent infrastructure, making demand extremely sticky.

The N2 node, beginning volume production in Q4 2025, will likely follow a similar pattern: Apple first, then NVIDIA and Broadcom dominate capacity, contributing more to TSMC profits.

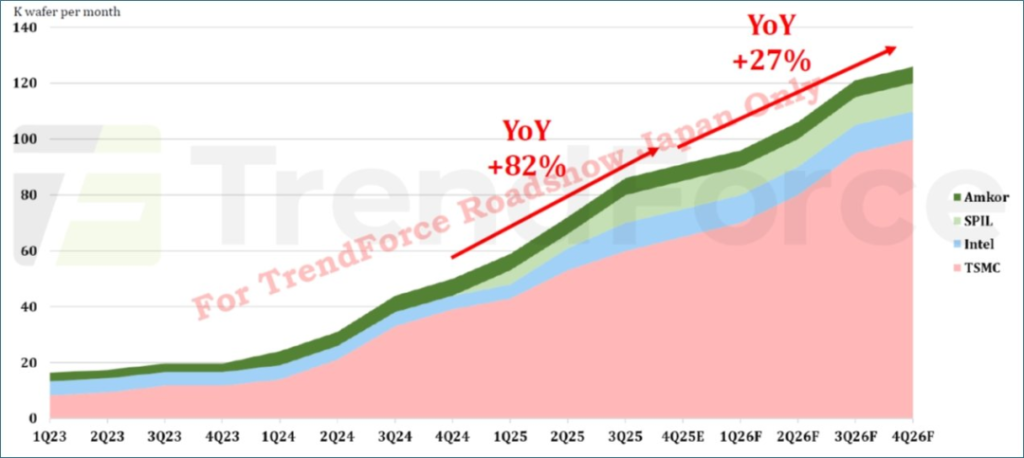

10. The Real Bottleneck Lies in CoWoS

AI semiconductor growth faces multiple bottlenecks, the most severe being 2.5D packaging capacity like CoWoS. Figure 14 shows 2.5D capacity trends. AI chips cannot rely solely on advanced process nodes—they require HBM integration, forming system-level integration, with CoWoS as the key.

Figure 14. Trend of 2.5D Packaging Capacity; Source: Joanne Chiao, TrendForce, “2026 Foundry Market Outlook – Advantages of Advanced Processes and Saturation of Mature Processes” (December 16, 2025) seminar materials.

If CoWoS capacity is insufficient, AI supply constraints cannot be resolved. However, if CoWoS bottlenecks are relieved, investment will not calm—it will intensify. Suppressed AI demand will surge, cloud providers will rush to purchase chips, expand AI data centers, and competition will intensify further. Investment will likely enter an even more aggressive phase.

11. Generative AI Semiconductor Trends Are Not a Bubble, But a Semiconductor “Tectonic Shift”

The conclusion is simple:

Cloud investment growth is driven by generative AI’s order-of-magnitude increase in computational demand;

This is not a bubble like Windows 95, IT, or memory bubbles, but a massive, strong AI trend;

Logic and memory markets continue to expand, with memory prices maintained at high levels due to AI transformation;

TSMC’s advanced nodes are fully occupied by AI, with N3’s main players shifting from Apple to NVIDIA and Broadcom;

The ultimate bottleneck is CoWoS, and once relieved, cloud investment will further accelerate, potentially “going into overdrive.”

Generative AI does not create a bubble—it creates a trend, triggering a “tectonic shift” in the semiconductor industry. Once the tectonic plates move, they cannot return to their original state.

FAQ

Q1: Is the AI investment surge a bubble? A1: No. It reflects an unprecedented, structural increase in computational demand, not speculative hype.

Q2: Why is cloud computing investment growing so fast? A2: Generative AI requires massive GPU-based computation, driving both infrastructure and hardware spending.

Q3: Will memory and logic chip prices remain high? A3: Yes. HBM and AI-specific logic chips are constrained by supply and essential for AI workloads, keeping prices elevated.

Generative AI Semiconductor Trends show how generative AI is reshaping computing demand, driving sustained growth in cloud and semiconductor markets.For manufacturers and integrators looking to source high-quality components to support AI, 7SEtronic can provide a wide range of electronic components, helping you meet these evolving requirements efficiently.