Introduction

NVIDIA Rubin BOM Analysis reveals a major shift in the economics of AI infrastructure. The AI server market is entering a new phase.

For years, NVIDIA GPUs captured most of the value inside AI infrastructure. However, the latest Morgan Stanley BOM analysis of NVIDIA’s upcoming Vera Rubin VR200 NVL72 platform suggests that the economics of AI hardware are changing rapidly.

For years, NVIDIA GPUs captured most of the value inside AI infrastructure. However, the latest Morgan Stanley BOM analysis of NVIDIA’s upcoming Vera Rubin VR200 NVL72 platform suggests that the economics of AI hardware are changing rapidly.

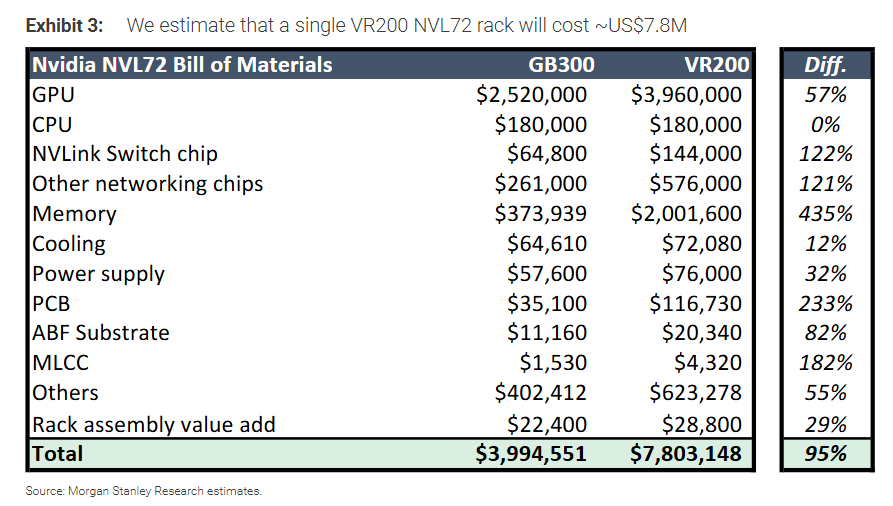

According to the report, the estimated ODM purchase price of a Vera Rubin rack reaches approximately US$7.8 million, nearly double the previous-generation GB300 platform at around US$4 million.

More importantly, the fastest-growing categories are no longer GPUs alone.

Memory value increases by 435%.

PCB content rises by 233%.

MLCC demand jumps by 182%.

Networking silicon grows by 121%.

As AI clusters become larger, denser, and more power-hungry, the supporting electronic components surrounding the GPU are becoming increasingly important.

For OEMs, EMS providers, industrial manufacturers, and procurement teams, understanding where this additional spending is flowing can provide valuable insight into future sourcing priorities, inventory planning, and supply chain risks.

Based on Morgan Stanley’s latest research and SemiAnalysis findings, this article breaks down the NVIDIA Vera Rubin VR200 NVL72 BOM structure and explores which electronic components are likely to benefit most from the next wave of AI infrastructure investment.

Rack Value Nearly Doubles: From US$4 Million to US$7.8 Million

Before diving into the details, let’s briefly review the platform itself.

The VR200 NVL72 is NVIDIA’s next-generation AI server platform based on the Vera Rubin architecture, first unveiled at CES. Each system integrates 72 Rubin GPUs and 36 Vera CPUs, with volume shipments expected to begin in the third quarter of 2026.

NVIDIA’s AI server roadmap currently follows this progression:

- Hopper (H100 / H200)

- Blackwell (GB200 / GB300)

- Vera Rubin (VR200)

According to Morgan Stanley’s NVIDIA Rubin BOM Analysis, the ODM purchase price of a VR200 NVL72 rack is approximately US$7.8 million, representing a 95% increase compared with the GB300 platform.

It is important to note that this figure represents the estimated rack value sold by ODM manufacturers rather than pure material cost. Therefore, the chart is better viewed as a value distribution model rather than a strict cost breakdown.

When examining the findings of the NVIDIA Rubin BOM Analysis, one trend becomes immediately clear:

The AI server supply chain is becoming significantly broader.

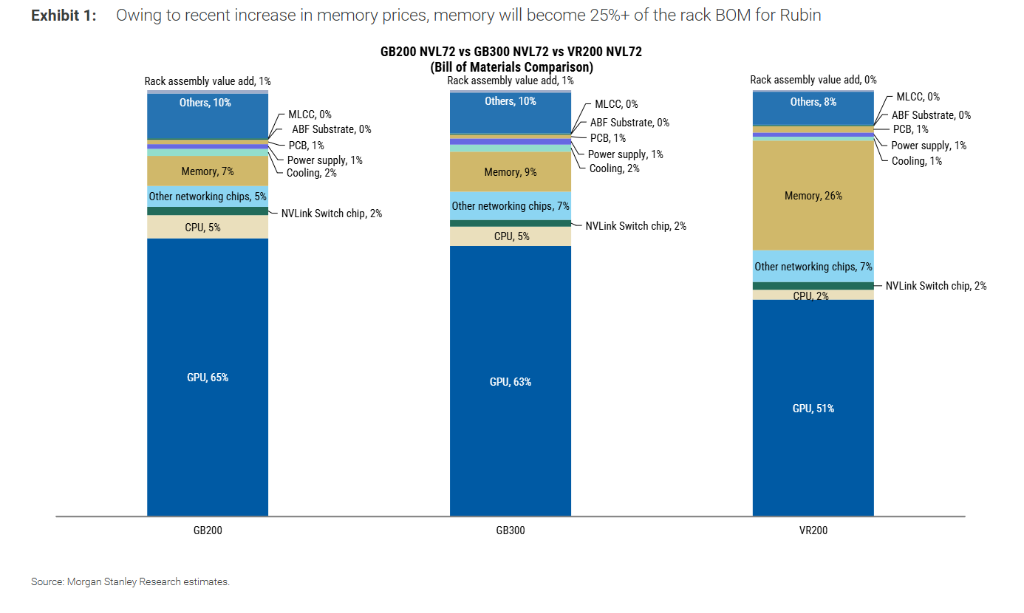

While GPUs remain the most valuable component category, their share of total rack value continues to decline as memory, networking, PCB, power systems, and passive components consume a larger portion of the budget.

This shift highlights how AI server components beyond the GPU are capturing an increasing share of system value, creating new opportunities for memory suppliers, PCB manufacturers, MLCC producers, power semiconductor vendors, and other electronic component suppliers.

Memory: The Largest Winner with 435% Growth

Memory is the fastest-growing category inside the Rubin platform.

SemiAnalysis notes that the “memory” category in Morgan Stanley’s report refers primarily to LPDDR5X SOCAMM modules and NVMe SSD storage. HBM is already included within the GPU value calculation.

The value of memory inside each rack rises from approximately US$370,000 in GB300 to nearly US$2 million in VR200, representing a remarkable 435% increase.

Two factors drive this growth.

Massive Increase in LPDDR5X Capacity

Each VR200 NVL72 rack contains approximately 54TB of LPDDR5X memory, more than three times the capacity of previous-generation systems.

SemiAnalysis estimates NVIDIA’s LPDDR5X procurement pricing at roughly US$8 per GB, creating hundreds of thousands of dollars in additional memory content per rack.

Large-Scale Adoption of 3D NAND Storage

The Rubin platform also introduces substantial PCIe storage capacity.

Reports suggest that each rack may contain over US$1 million worth of 3D NAND storage, a category that contributed very little value in previous systems.

Related Component Suppliers

Several memory suppliers are positioned to benefit from the Rubin ecosystem:

- Samsung

- SK Hynix

- Micron

These companies are expected to provide HBM4, LPDDR5X SOCAMM2 modules, and PCIe Gen6 SSD products supporting future AI server deployments.

GPU and CPU: Still Dominant but Losing Share

According to the NVIDIA Rubin BOM Analysis, GPUs continue to dominate total system value, but their percentage contribution is gradually shrinking.

Each Rubin GPU is estimated to cost approximately US$55,000. With 72 GPUs per rack, total GPU value approaches US$4 million.

However, GPU contribution drops from roughly 63% of total rack value in GB300 to around 51% in VR200.

Meanwhile, CPU spending remains relatively stable.

The Rubin platform continues NVIDIA’s established 1:2 CPU-to-GPU ratio, deploying 36 Vera CPUs alongside 72 Rubin GPUs.

One of the most important findings from the NVIDIA Rubin BOM Analysis is that growth is increasingly shifting toward supporting AI server components rather than GPUs alone. Memory, networking devices, PCB assemblies, power systems, and passive electronic components are capturing a larger share of overall system value.

This trend suggests that future AI infrastructure spending may create opportunities across a much broader electronic components supply chain, extending well beyond NVIDIA’s processors.

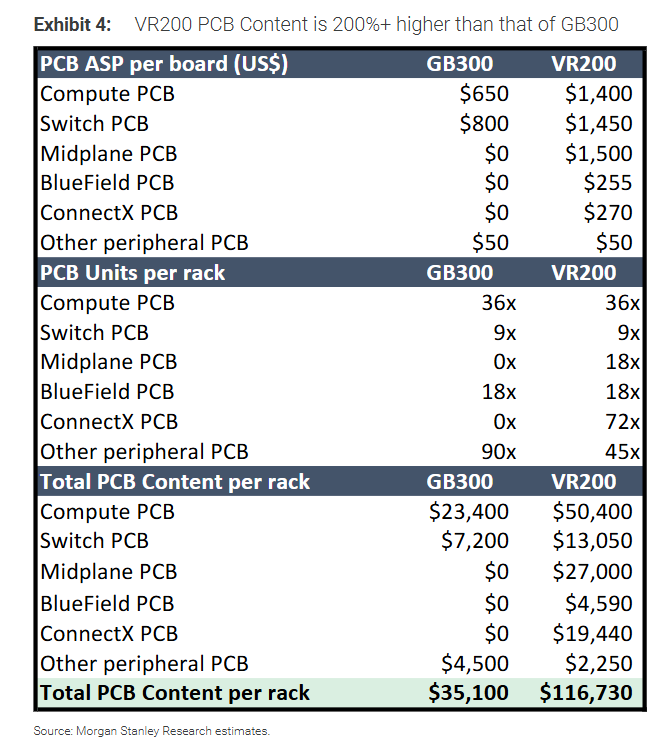

PCB: Up 233% as Board Complexity Increases

After memory, PCB is one of the largest beneficiaries of the Rubin architecture.

PCB value increases from approximately US$35,100 in GB300 to US$116,700 in VR200, representing growth of roughly 233%.

Several design changes contribute to this increase.

New PCB Categories

Rubin introduces:

- ConnectX module PCBs

- Midplane PCBs

These boards did not exist in previous generations and contribute more than US$46,000 in additional content value per rack.

Higher Layer Counts

Existing boards also become significantly more complex.

Examples include:

- Compute boards increasing from 22-layer to 26-layer designs

- Switch tray PCBs expanding from 24 layers to 32 layers

- New 44-layer midplane boards added to compute trays

As signal integrity requirements continue rising, higher-end PCB materials and manufacturing technologies become necessary.

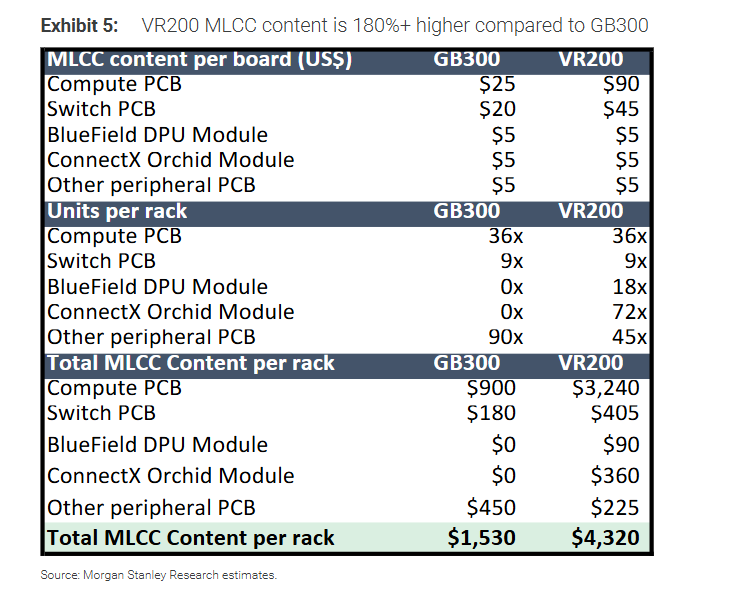

MLCC: Demand Growth Accelerates

Although MLCCs represent a relatively small percentage of total rack value, their growth rate is substantial.

MLCC content increases from approximately US$1,530 in GB300 to roughly US$4,320 in VR200, representing growth of approximately 182%.

The primary drivers are:

Higher MLCC Content per Board

Compute board MLCC value rises from approximately US$25 to US$90.

Switch board MLCC value more than doubles as well.

Additional Modules Increase Consumption

The introduction of:

- 18 BlueField DPU modules

- 72 ConnectX modules

creates significant additional demand for server-grade MLCCs.

Morgan Stanley also notes that ODM manufacturers are actively building inventory ahead of Rubin production ramps expected in late 2026.

Potential MLCC Supply Challenges

Historically, MLCC shortages have emerged whenever major technology transitions occur.

As AI infrastructure spending accelerates, procurement teams may face increasing pressure in securing high-performance MLCCs used for power delivery, signal filtering, and networking applications.

Related Component Suppliers

Industry research suggests that the high-end AI server MLCC market is dominated by:

- Murata

- Samsung Electro-Mechanics

- Taiyo Yuden

- Kyocera

These suppliers collectively account for the majority of high-performance MLCC production capacity worldwide.

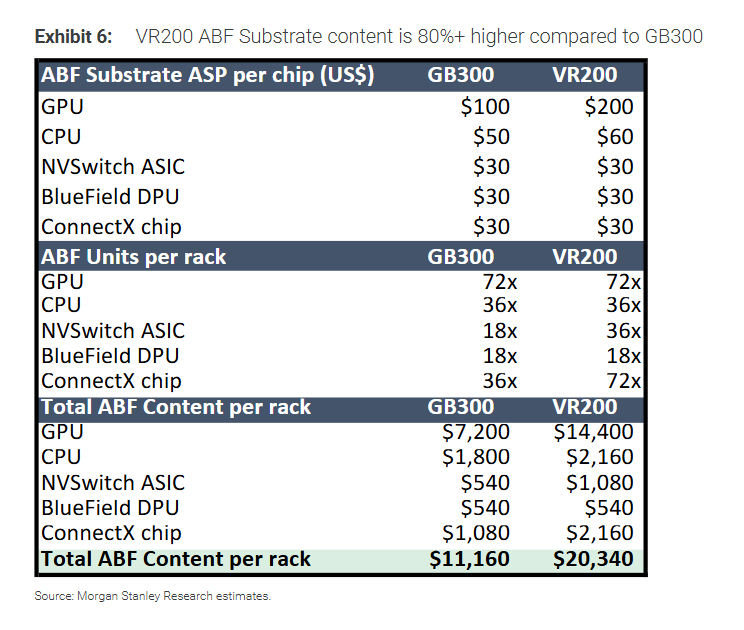

ABF Substrates: Up 82%

ABF substrate value increases from approximately US$11,200 to US$20,300 per rack.

Several factors contribute:

- Rubin GPU substrate pricing nearly doubles

- NVSwitch ASIC count doubles

- ConnectX chip count doubles

As advanced packaging becomes increasingly important, ABF substrate suppliers are expected to remain critical participants in the AI supply chain.

Power Systems: 800V HVDC Is the Next Big Shift

Power system value rises approximately 32% in the Rubin platform.

However, the bigger story is the transition toward high-voltage direct current (HVDC) architecture.

Industry reports indicate that certain hyperscale cloud providers are already testing dedicated 800V HVDC power racks alongside Vera Rubin deployments.

NVIDIA has publicly announced plans to support large-scale 800V HVDC architecture across future AI infrastructure generations.

Related Semiconductor Suppliers

NVIDIA’s official ecosystem includes power semiconductor partners such as:

- Analog Devices

- Infineon

- Innoscience

- MPS

- Navitas

- Onsemi

- Renesas

- ROHM

- STMicroelectronics

- Texas Instruments

As rack power requirements continue climbing, demand for power management ICs, GaN devices, SiC devices, and high-efficiency power conversion solutions is expected to grow significantly.

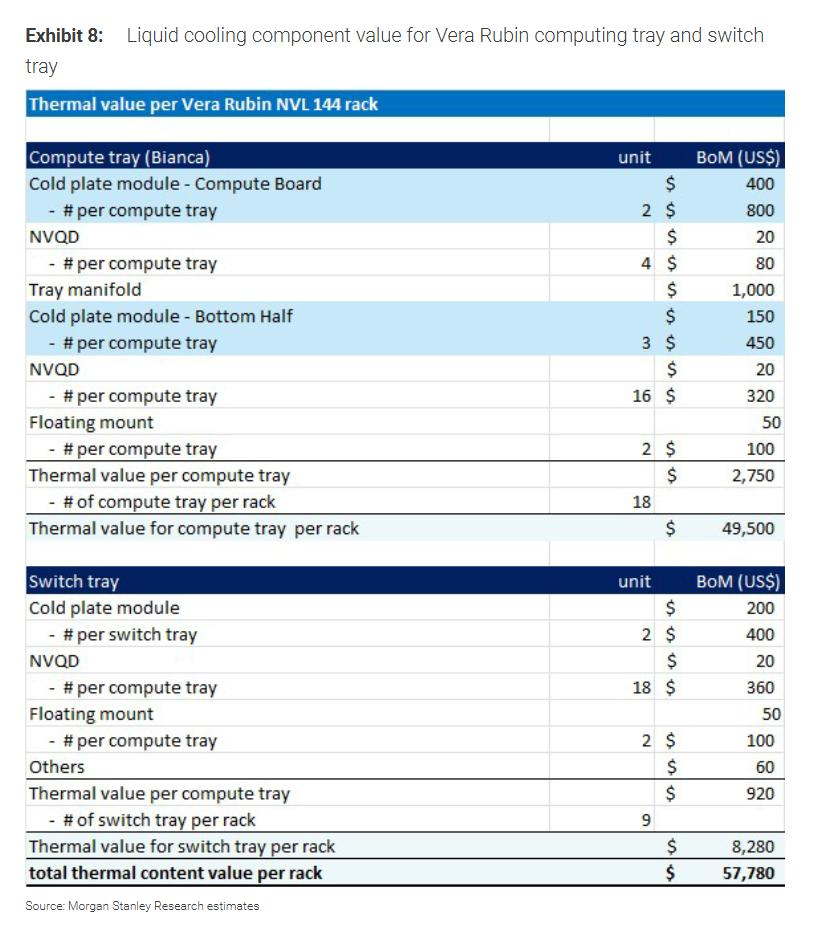

Cooling: Liquid Cooling Becomes Standard

Cooling content value rises approximately 12%.

More importantly, Rubin fully transitions to liquid cooling architecture.

Traditional server fans are eliminated entirely.

As rack power exceeds 100kW, liquid cooling is increasingly becoming a necessity rather than an option.

This transition is expected to create additional opportunities for cooling system suppliers, liquid distribution components, connectors, sensors, and thermal management technologies.

What This Means for Electronic Component Buyers

While most industry headlines focus on NVIDIA GPUs, the Rubin BOM structure tells a broader story.

The fastest-growing categories are not necessarily processors.

They are the supporting electronic components that enable next-generation AI infrastructure.

| Component Category | Growth vs GB300 |

|---|---|

| Memory | +435% |

| PCB | +233% |

| MLCC | +182% |

| ABF Substrate | +82% |

| Power Systems | +32% |

For procurement teams, OEMs, and EMS providers, these trends highlight the importance of monitoring supply availability long before large-scale production begins.

As hyperscalers and ODM manufacturers continue securing future capacity, lead times and pricing volatility may become increasingly important considerations.

Final Thoughts

The NVIDIA Rubin BOM analysis reveals a significant shift in AI infrastructure economics.

Although GPUs remain the largest value contributor, their share of total rack value continues to decline as memory, PCB, networking, power delivery, and passive components account for an increasing portion of overall spending.

For the electronic components industry, this suggests that future AI growth may benefit a much broader supplier ecosystem than previous generations.

As production ramps toward 2026 and 2027, demand for server-grade MLCCs, advanced PCB materials, ABF substrates, power semiconductors, connectors, and memory products is likely to remain strong.

For OEMs, EMS companies, and industrial equipment manufacturers, understanding these trends early can help reduce sourcing risks and improve long-term procurement planning.

At 7SEtronic, we continuously monitor component availability across global supply chains and support customers with sourcing, BOM fulfillment, hard-to-find components, PCBA support and long-term procurement strategies.

As the Rubin generation approaches mass deployment, staying ahead of component market shifts may become a competitive advantage for manufacturers across the electronics industry.

FAQ

Q1. Why is memory growing faster than GPUs in NVIDIA Rubin servers?

Because Rubin significantly increases LPDDR5X capacity and introduces large-scale 3D NAND storage, dramatically increasing memory content per rack.

Q2. Which electronic components may benefit most from Rubin deployments?

Memory, MLCCs, advanced PCBs, ABF substrates, power semiconductors, connectors, and networking devices are among the largest beneficiaries.

Q3. Could AI server demand create future component shortages?

Potentially yes. High-end MLCCs, advanced substrates, memory products, and power devices could face supply pressure as AI infrastructure spending accelerates.

Others also view:

- NVIDIA Rubin BOM Analysis: What Component Buyers Need to Know Before the Next AI Hardware Wave

- Semiconductor Traceability vs Date Code: Can Older IC Inventory Still Be Reliable?

- From Components Sourcing to PCB Assembly: How 7SEtronic Supports OEM & EMS Projects

- Infineon Earnings Report: What OEM and EMS Buyers Need to Know About the 2026 Chip Market

- ICM-42688-P Price Surge Explained: From 9 RMB to 100 RMB and Back