Introduction

Multilayer Ceramic Capacitors (MLCCs) are among the most essential components in modern electronics.

From smartphones and industrial equipment to electric vehicles, AI servers, telecommunications infrastructure, renewable energy systems, and medical devices, MLCCs play a critical role in power management, signal filtering, and system stability.

As artificial intelligence, automotive electrification, and industrial automation continue driving global electronics demand, procurement teams are paying closer attention to supplier capabilities, financial health, product reliability, and supply chain resilience.

In this article, we review twelve leading global MLCC manufacturers based on their latest financial performance and market positioning while exploring the key trends shaping the MLCC industry in 2026.

Top 12 MLCC Manufacturers at a Glance

| Company | Headquarters | Revenue | Gross Margin |

|---|---|---|---|

| Murata Manufacturing | Japan | JPY 1.83 Trillion | 42.3% |

| TDK | Japan | JPY 2.50 Trillion | 31.3% |

| Kyocera | Japan | JPY 2.07 Trillion | 29.4% |

| Samsung Electro-Mechanics | South Korea | KRW 11.31 Trillion | 20.1% |

| Taiyo Yuden | Japan | JPY 355.3 Billion | 23.1% |

| Yageo | Taiwan | TWD 132.9 Billion | 36.2% |

| Walsin Technology | Taiwan | TWD 36.5 Billion | 17.3% |

| Three-Circle Group | China | RMB 9.01 Billion | 42.1% |

| Fenghua Advanced Technology | China | RMB 5.76 Billion | 17.8% |

| Torch Electron | China | RMB 4.12 Billion | 27.1% |

| Hongyuan Electronics | China | RMB 1.79 Billion | 44.4% |

| Dalicap Technology | China | RMB 362 Million | 66.2% |

Global MLCC Market Structure

The global MLCC industry remains highly concentrated, with a small group of manufacturers controlling the majority of production capacity, technology leadership, and automotive-grade certifications.

Tier 1 Global Leaders

- Murata Manufacturing

- Samsung Electro-Mechanics

- TDK

These companies dominate premium applications such as AI servers, automotive electronics, telecommunications infrastructure, and industrial automation.

Tier 2 Global Suppliers

- Yageo

- Kyocera

- Taiyo Yuden

- Walsin Technology

These suppliers offer strong alternatives for industrial, networking, consumer electronics, and automotive applications.

Emerging Chinese Suppliers

- Three-Circle Group

- Fenghua Advanced Technology

- Torch Electron

- Hongyuan Electronics

- Dalicap Technology

Chinese manufacturers continue improving technology, profitability, and manufacturing capabilities while expanding their presence in global supply chains.

Top 12 MLCC Manufacturers Analysis

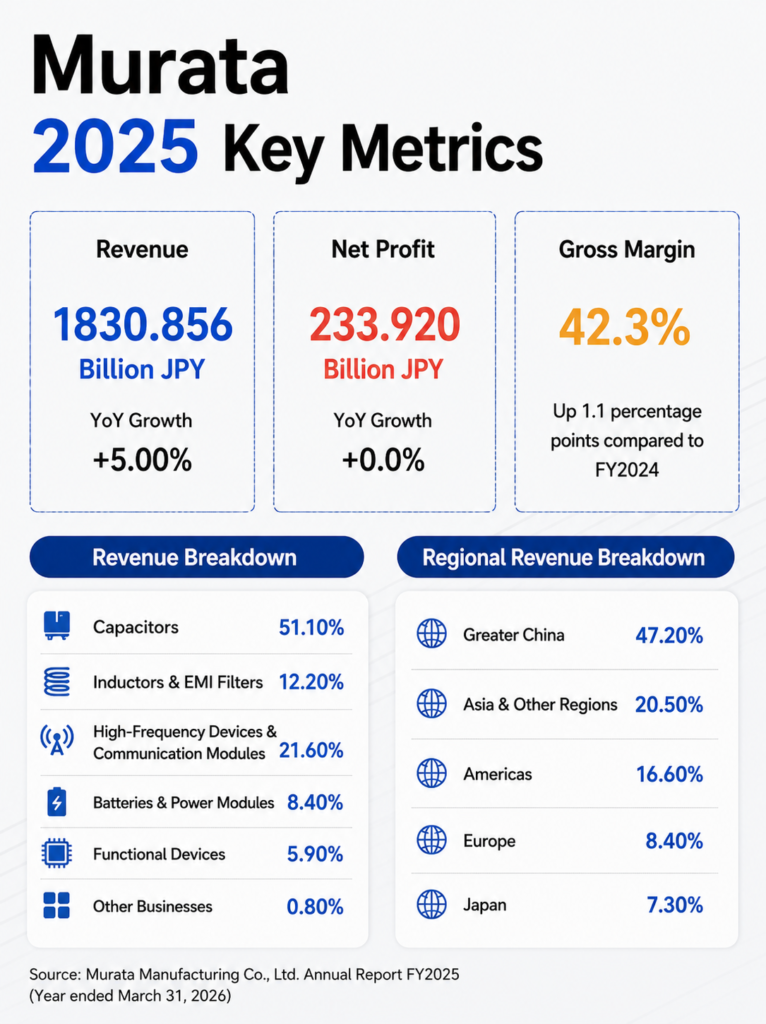

1. Murata Manufacturing

Founded in 1944 and headquartered in Kyoto, Japan, Murata Manufacturing is widely recognized as the global leader in MLCC technology and production capacity. The company supplies advanced passive components to industries including smartphones, automotive electronics, telecommunications infrastructure, industrial automation, cloud computing, and AI platforms.

Financial Performance

- Revenue: JPY 1.83 trillion

- Revenue Growth: +5.0% YoY

- Net Profit: JPY 233.9 billion

- Gross Margin: 42.3%

Murata remains the world’s largest MLCC manufacturer and continues to maintain industry-leading profitability.

Market Perspective

Murata continues to set the benchmark for the global MLCC industry. Its industry-leading margin reflects strong pricing power, advanced materials technology, and leadership in high-value segments such as automotive electronics, AI infrastructure, and telecommunications equipment.

As electronic devices become smaller and more power-intensive, Murata remains one of the few suppliers capable of consistently delivering high-capacitance and ultra-miniature MLCC products at scale.

2. TDK Corporation

Founded in 1935 and headquartered in Tokyo, Japan, TDK is one of the world’s most diversified electronic component manufacturers. Its portfolio includes MLCCs, sensors, batteries, magnetic materials, and power solutions.

Financial Performance

- Revenue: JPY 2.50 trillion

- Revenue Growth: +13.6% YoY

- Net Profit: JPY 195.7 billion

- Gross Margin: 31.3%

TDK delivered one of the strongest growth rates among major MLCC suppliers.

Market Perspective

TDK delivered one of the strongest growth performances among major MLCC suppliers during the latest fiscal year.

Its diversified business portfolio reduces dependence on any single market segment, while growing exposure to electric vehicles, industrial automation, and energy infrastructure provides long-term growth opportunities beyond traditional consumer electronics.

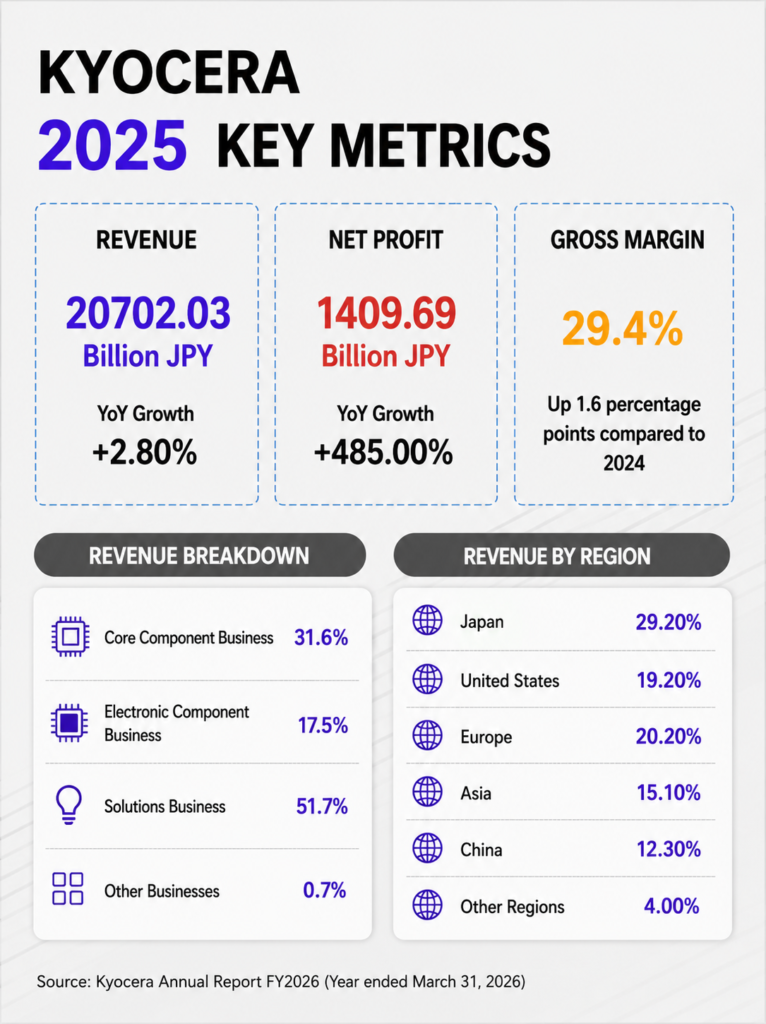

3. Kyocera Corporation

Founded in 1959 and headquartered in Kyoto, Japan, Kyocera is a leading manufacturer of advanced ceramics, semiconductor packaging, electronic components, and industrial equipment.

Financial Performance

- Revenue: JPY 2.07 trillion

- Revenue Growth: +2.8% YoY

- Net Profit: JPY 141.0 billion

- Net Profit Growth: +485.0% YoY

- Gross Margin: 29.4%

Kyocera achieved a significant recovery in profitability during the fiscal year.

Market Perspective

Kyocera’s strength comes from its deep expertise in advanced ceramic materials, which form the foundation of many high-reliability electronic components.

Although MLCCs represent only part of its broader business portfolio, the company remains a trusted supplier for industrial, aerospace, and automotive applications where long-term reliability is often prioritized over cost.

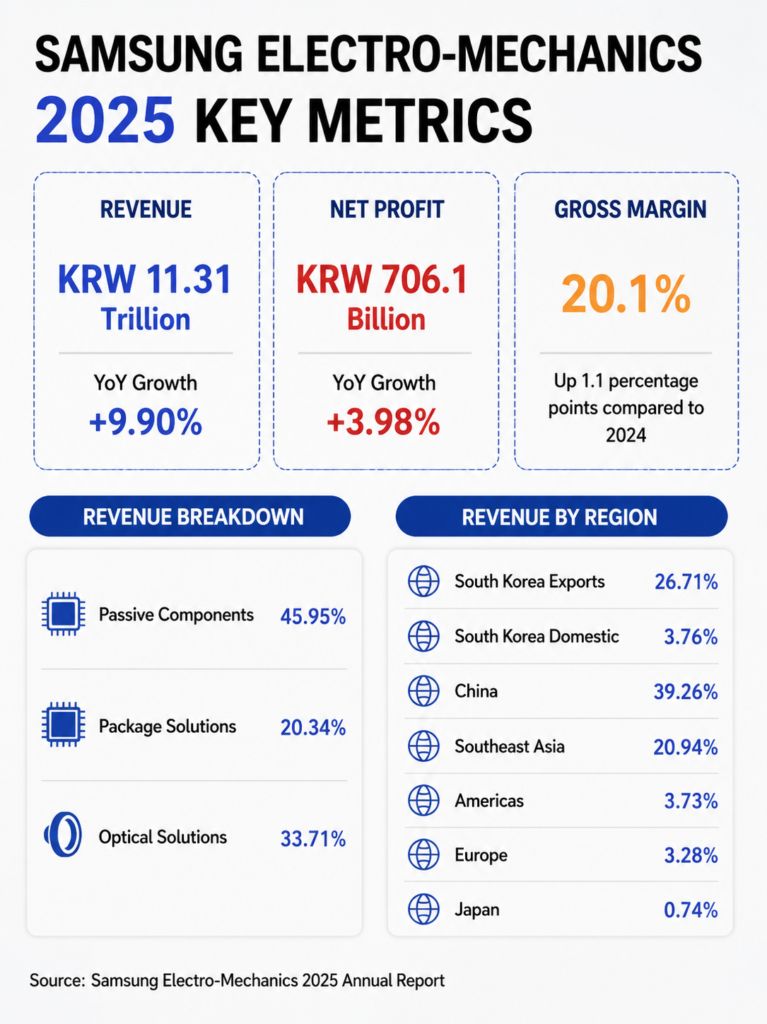

4. Samsung Electro-Mechanics

Founded in 1973 and headquartered in Suwon, South Korea, Samsung Electro-Mechanics is one of the world’s largest MLCC manufacturers. The company also produces semiconductor substrates and camera modules.

Financial Performance

- Revenue: KRW 11.31 trillion

- Revenue Growth: +9.9% YoY

- Net Profit: KRW 706.1 billion

- Gross Margin: 20.1%

Samsung continued benefiting from growing demand in automotive electronics and high-performance computing.

Market Perspective

Samsung Electro-Mechanics remains one of the few manufacturers capable of competing directly with Murata in high-capacitance MLCC applications.

The company’s recent growth has been supported by increasing demand from automotive electronics and AI-related computing platforms. Continued investment in automotive-grade MLCC production is expected to strengthen Samsung’s position in higher-margin markets over the coming years.

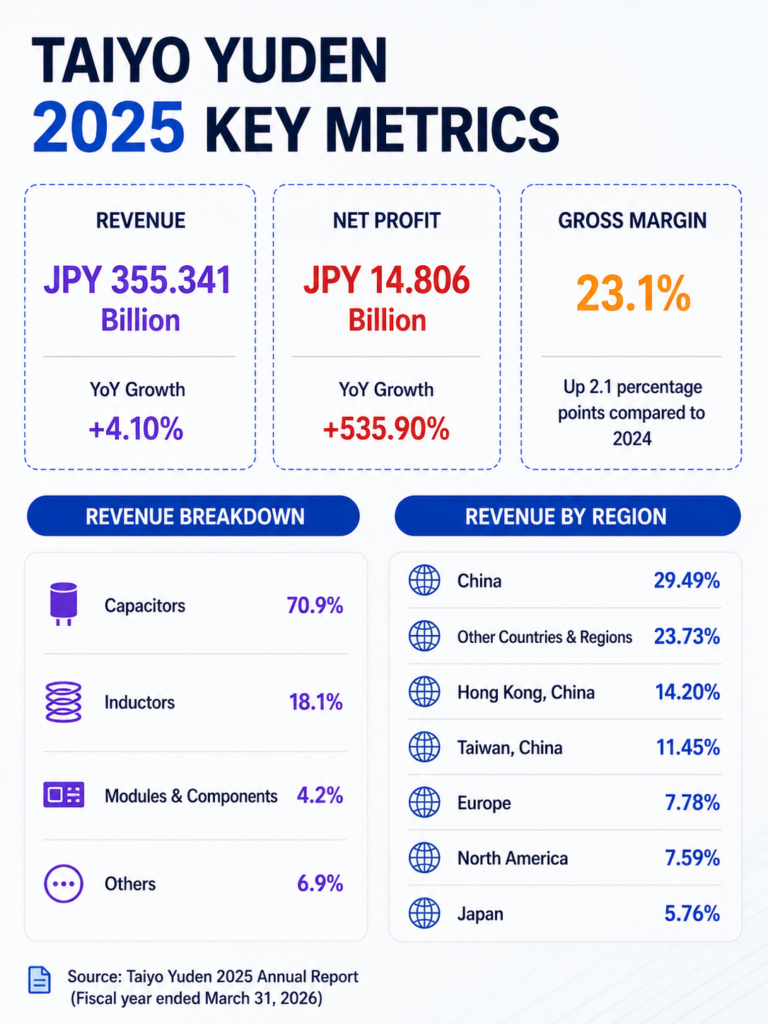

5. Taiyo Yuden

Founded in 1950 and headquartered in Tokyo, Japan, Taiyo Yuden is one of the pioneers of modern MLCC technology. The company maintains strong positions in communications, automotive electronics, and high-frequency applications.

Financial Performance

- Revenue: JPY 355.3 billion

- Revenue Growth: +4.1% YoY

- Net Profit: JPY 14.8 billion

- Net Profit Growth: +535.9% YoY

- Gross Margin: 23.1%

Taiyo Yuden experienced a strong recovery in profitability.

Market Perspective

Taiyo Yuden remains one of the industry’s most respected MLCC manufacturers, particularly in communications and high-frequency applications.

Its strong profit recovery suggests improving demand conditions in both automotive and wireless communication markets. The company continues to benefit from increasing connectivity requirements across modern electronic systems.

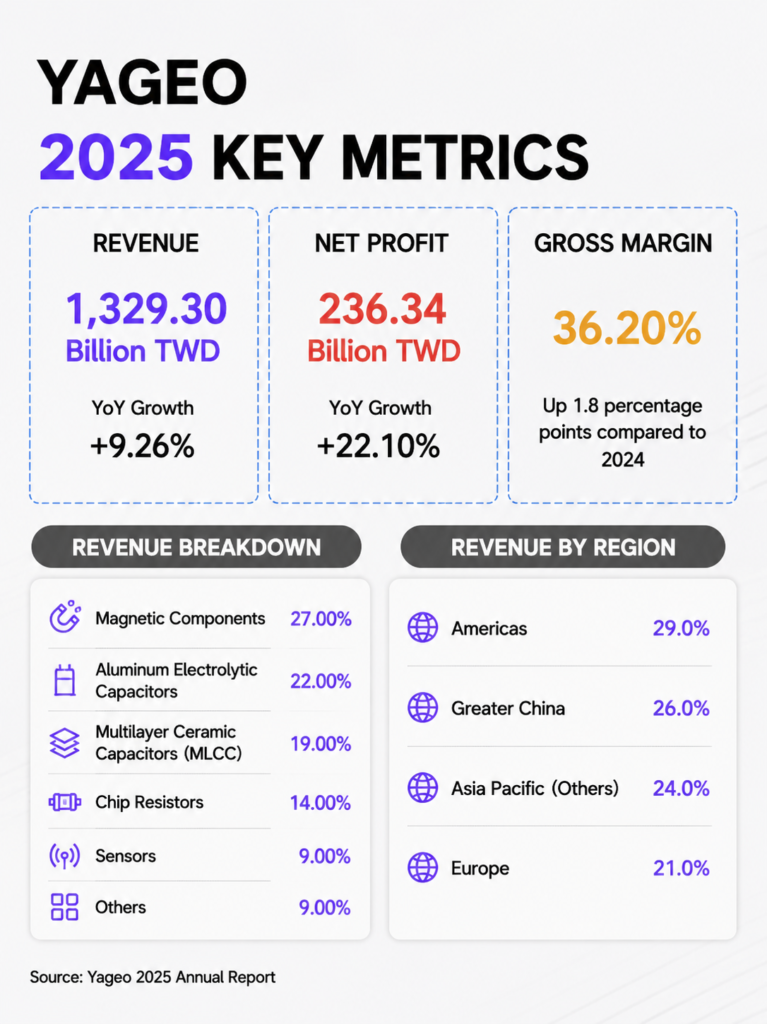

6. Yageo Corporation

Founded in 1977 and headquartered in Taiwan, Yageo has become one of the world’s largest passive component suppliers. Following acquisitions such as KEMET, the company significantly expanded its global presence.

Financial Performance

- Revenue: TWD 132.9 billion

- Revenue Growth: +9.26% YoY

- Net Profit: TWD 23.63 billion

- Net Profit Growth: +22.1% YoY

- Gross Margin: 36.2%

Yageo continues delivering strong profitability and balanced growth.

Market Perspective

Yageo has successfully transformed itself from a passive component supplier into a global electronic component group through strategic acquisitions such as KEMET.

Today, the company offers one of the broadest passive component portfolios in the industry and is increasingly viewed as a strong alternative to traditional Japanese suppliers, particularly for industrial, automotive, and networking applications.

7. Walsin Technology

Founded in 1992 and headquartered in Taiwan, Walsin Technology is one of Asia’s major passive component manufacturers.

Financial Performance

- Revenue: TWD 36.46 billion

- Revenue Growth: +4.91% YoY

- Net Profit: TWD 2.30 billion

- Net Profit Growth: -22.95% YoY

- Gross Margin: 17.28%

Walsin remains a significant supplier despite profitability pressure.

Market Perspective

Walsin continues to maintain a strong position in the global passive component market despite profitability challenges.

The company’s manufacturing scale, broad product availability, and competitive pricing make it an attractive option for customers seeking cost-effective sourcing solutions and secondary supplier qualification programs.

8. Three-Circle Group (CCTC)

Founded in 1970 and headquartered in Guangdong, China, Three-Circle Group is widely regarded as China’s leading electronic ceramics manufacturer.

Its business spans MLCCs, ceramic substrates, optical communication components, and advanced ceramic materials.

Financial Performance

- Revenue: RMB 9.01 billion

- Revenue Growth: +22.13% YoY

- Net Profit: RMB 2.62 billion

- Net Profit Growth: +19.54% YoY

- Gross Margin: 42.14%

Three-Circle delivered one of the strongest financial performances among Chinese MLCC manufacturers.

Market Perspective

Three-Circle is widely regarded as China’s most competitive MLCC manufacturer.

Perhaps the most noteworthy indicator is its gross margin of 42.14%, which is already approaching Murata’s 42.3%. This highlights the company’s strong manufacturing efficiency and growing technological capabilities.

As China continues investing in supply chain localization, Three-Circle is well positioned to benefit from increasing domestic demand and qualification opportunities.

Interesting Observation

Three-Circle’s gross margin reached 42.14% in 2025, nearly matching Murata’s 42.3%.

While profitability alone does not determine technological leadership, it highlights how rapidly Chinese MLCC manufacturers are improving manufacturing efficiency and product competitiveness.

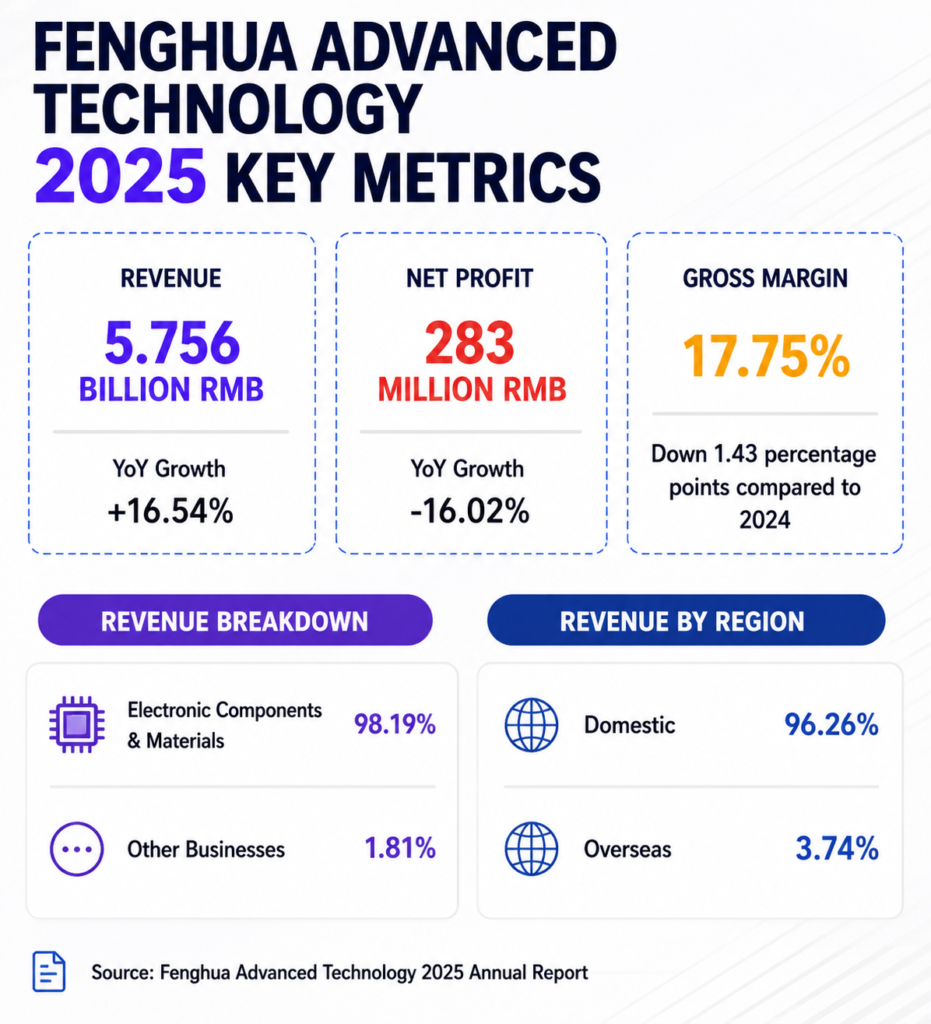

9. Fenghua Advanced Technology

Founded in 1984 and headquartered in Guangdong, China, Fenghua is one of China’s earliest MLCC manufacturers.

Financial Performance

- Revenue: RMB 5.76 billion

- Revenue Growth: +16.54% YoY

- Net Profit: RMB 283 million

- Net Profit Growth: -16.02% YoY

- Gross Margin: 17.75%

Revenue growth remained healthy despite ongoing margin pressure.

Market Perspective

As one of China’s earliest MLCC manufacturers, Fenghua continues to play an important role in the domestic passive component market.

While profitability remains under pressure due to intense competition, the company’s revenue growth demonstrates that demand for domestic alternatives continues to expand across consumer, industrial, and automotive applications.

10. Torch Electron

Founded in 1989 and headquartered in Fujian, China, Torch Electron specializes in high-reliability capacitors and military-grade electronic components.

Financial Performance

- Revenue: RMB 4.12 billion

- Revenue Growth: +47.09% YoY

- Net Profit: RMB 320 million

- Net Profit Growth: +64.39% YoY

- Gross Margin: 27.13%

Torch recorded one of the fastest growth rates among all companies reviewed.

Market Perspective

Torch Electron recorded one of the highest growth rates among all companies reviewed.

Its strong position in aerospace, defense, and high-reliability applications provides greater resilience against pricing pressure compared with suppliers focused primarily on consumer electronics.

The company continues benefiting from growing demand for domestically sourced high-reliability components.

11. Hongyuan Electronics

Founded in 2001 and headquartered in Beijing, China, Hongyuan focuses on high-reliability MLCCs and microwave electronic components.

Financial Performance

- Revenue: RMB 1.79 billion

- Revenue Growth: +20.28% YoY

- Net Profit: RMB 250 million

- Net Profit Growth: +62.54% YoY

- Gross Margin: 44.39%

Hongyuan maintained excellent profitability through its focus on specialized markets.

Market Perspective

Hongyuan’s strong profitability reflects the attractive economics of specialized high-reliability electronic components.

By focusing on aerospace, defense, and mission-critical communications systems, the company has established higher technical barriers and stronger margins than many volume-oriented passive component manufacturers.

12. Dalicap Technology

Founded in 2011 and headquartered in Dalian, China, Dalicap focuses on high-frequency ceramic capacitors for RF, microwave, and communication applications.

Financial Performance

- Revenue: RMB 362 million

- Revenue Growth: +12.07% YoY

- Net Profit: RMB 159 million

- Net Profit Growth: +39.88% YoY

- Gross Margin: 66.17%

Dalicap achieved the highest gross margin among all companies reviewed.

Market Perspective

Although Dalicap is significantly smaller than the industry’s major players, it achieved the highest gross margin among all companies reviewed.

This demonstrates the profitability potential of specialized RF and microwave capacitor markets, where technical expertise often matters more than production scale.

As 5G, satellite communications, and advanced wireless systems continue expanding, Dalicap is positioned to benefit from growing demand for high-frequency components.

Are Chinese MLCC Manufacturers Closing the Gap?

Chinese suppliers have made remarkable progress over the past decade.

Key Advantages

- Competitive manufacturing costs

- Faster domestic delivery

- Strong local supply chain ecosystem

- Expanding automotive and industrial certifications

Remaining Challenges

- Ultra-miniature package technologies (01005 and below)

- Premium automotive-grade products

- Long-term reliability validation

- High-capacitance flagship products

While Japanese manufacturers continue leading the highest-end segments, Chinese suppliers are becoming increasingly attractive alternatives for industrial and consumer electronics.

AI Infrastructure Is Creating a New Wave of MLCC Demand

Modern AI servers require significantly more MLCCs than traditional enterprise servers.

MLCCs are extensively used in:

- GPU power delivery systems

- CPU voltage regulation modules

- High-speed networking equipment

- Memory subsystems

- Server power supplies

As global investment in AI infrastructure accelerates, demand for high-performance MLCCs is expected to remain strong throughout 2026 and beyond.

Automotive Electronics Continue to Drive Growth

Vehicle electrification has significantly increased MLCC consumption per vehicle.

- Traditional Internal Combustion Vehicles: 3,000-5,000 MLCCs

- Electric Vehicles: 8,000-15,000 MLCCs

- Advanced ADAS Platforms: Even higher

This trend continues to support demand for automotive-qualified MLCC products.

MLCC Manufacturer Selection Guide

| Application | Recommended Suppliers |

|---|---|

| AI Servers & Data Centers | Murata, Samsung Electro-Mechanics, TDK |

| Automotive Electronics | Murata, TDK, Taiyo Yuden |

| Industrial Automation | Yageo, Kyocera, Walsin |

| Consumer Electronics | Yageo, Walsin, Fenghua |

| Telecommunications Equipment | Murata, TDK, Taiyo Yuden |

| RF & Microwave Applications | Dalicap, Murata |

| Aerospace & Defense | Torch Electron, Hongyuan Electronics |

| Cost-Sensitive Projects | Fenghua, Walsin, Yageo |

| China Localization Projects | Three-Circle, Fenghua, Torch Electron |

How 7SEtronic Supports MLCC Sourcing

Selecting the right MLCC manufacturers is only part of the challenge.

Many procurement teams also face:

- Long lead times

- Sudden allocation

- EOL notifications

- BOM cost reduction targets

- Alternative part qualification

- Price volatility

- Multi-supplier management

At 7SEtronic, we support OEMs, EMS providers, industrial equipment manufacturers, and product development teams through:

MLCC Sourcing Support

Access to global inventory channels covering both mainstream and hard-to-find MLCC products.

Alternative Recommendations

Cross-reference support when original manufacturers face shortages, allocation, or long lead times.

BOM Cost Optimization

Helping customers identify opportunities to reduce procurement costs while maintaining performance requirements.

Supply Chain Risk Management

Supporting supplier diversification strategies and backup sourcing plans to improve business continuity.

Components Sourcing + PCBA Support

Beyond electronic component sourcing, 7SEtronic also provides PCB and PCBA support, helping customers simplify procurement processes and reduce supplier management complexity.

Final Thoughts

The global MLCC market continues to evolve alongside AI infrastructure, automotive electrification, and industrial automation.

While Murata, Samsung Electro-Mechanics, TDK, and Yageo remain dominant global suppliers, Chinese manufacturers such as Three-Circle, Fenghua, Torch Electron, Hongyuan, and Dalicap are steadily improving their competitiveness and expanding their presence in global supply chains.

For procurement professionals, evaluating technology capability, financial stability, qualification status, and supply chain resilience is becoming just as important as comparing prices.

In an increasingly dynamic market, building a flexible sourcing strategy and maintaining qualified alternative suppliers may be one of the most effective ways to reduce risk and ensure long-term supply continuity.

FAQ

Are Chinese MLCC manufacturers catching up with Japanese suppliers?

Chinese MLCC manufacturers such as Three-Circle, Fenghua, and Torch Electron have made significant progress in manufacturing capability and product quality. While Japanese MLCC manufacturers still lead in certain premium segments, Chinese suppliers are becoming increasingly competitive in industrial and consumer electronics markets.

Why is demand for MLCC manufacturers expected to grow in 2026?

Demand for MLCC manufacturers is being driven by AI infrastructure, electric vehicles, industrial automation, and advanced communications equipment. These applications require significantly more MLCCs than traditional electronic products, supporting long-term market growth.

Will AI and EV demand affect MLCC manufacturers’ pricing and lead times?

Yes. Growing demand from AI servers, electric vehicles, and industrial automation is increasing consumption of high-performance MLCCs. As a result, some MLCC manufacturers may experience capacity constraints, leading to higher prices and longer lead times for certain automotive-grade and high-capacitance products.compared to standard components

Others also view:

- How the AI Server Supply Chain Is Reshaping PCB, MLCC, Copper Foil and Electronic Glass Fiber Markets

- Top 12 Global MLCC Manufacturers in 2026: Financial Performance, Market Position and Supply Chain Trends

- NVIDIA Rubin BOM Analysis: What Component Buyers Need to Know Before the Next AI Hardware Wave

- Semiconductor Traceability vs Date Code: Can Older IC Inventory Still Be Reliable?

- From Components Sourcing to PCB Assembly: How 7SEtronic Supports OEM & EMS Projects